Member states of the Monetary Union need rules to manage their public finances. A situation without any rules would probably be the worst option. However, there has been criticism of the existing EU rules. Could the EU change its fiscal rules so that they could make fiscal policy less pro-cyclical and enhance debt sustainability?

Authors

Arto Kokkinen

Senior Economist, PhD

Monitoring and Oversight

Matthias Strifler

Senior Economist, PhD

Monitoring and Oversight

They will start this autumn: The negotiations between EU Member States on fiscal policy rules.

As a result of the COVID-19 pandemic, the debt ratios of many EU countries are now well above the 60 per cent limit. Returning to the old rules may be difficult. Under the existing rules, a Member State’s general government deficit-to-GDP ratio should not exceed 3% while the public debt-to-GDP ratio should stay below 60%. These rules have been criticised for several reasons.

It has been pointed out that the existing rules encourage governments to pursue a fiscal policy widening cyclical fluctuations even though they are expected to have the opposite effect. Moreover, despite the rules, the debt ratios of both the Member States and the euro area as a whole have deteriorated and the sustainability of public finances has weakened. The rules do not provide any incentive to build fiscal buffers for a downturn during a period of rapid economic growth.

As recently as two years ago, researchers and experts proposed that the rules should be simplified and changed so that fiscal policy would not widen cyclical fluctuations. Because of growing debts, the focus was on the debt rule.

Over the past year, the debate on changing the rules has died down. It has been reported that there are disagreements between EU Member States. Countries with high debt ratios feel that the current 60 per cent limit is too strict, while countries with low debt ratios fear that high-debt countries are seeking to relax the existing debt rule. This means that not all countries are prepared to open the Treaty on European Union (Maastricht Treaty) concluded in 1992 for revision. The three per cent deficit rule and the 60 per cent debt rule referred to above are based on this treaty. However, it is to be hoped that the debate on EU rules would move beyond an argument over the current debt/GDP benchmark.

Is the EU missing its opportunity to improve its own fiscal rules? Is it worth making any new proposals?

Finally, it is the Member States that make the decisions. It is quite possible that they will end up in a compromise as so many times before. For this reason, we should be prepared for negotiations in which concrete proposals for new rules are presented. Below we present one such proposal and at the end of this blog, we consider alternatives to it.

Balance is the difference between general government revenue and expenditure. When expenditure exceeds revenue, the resulting deficit boosts debts. Correspondingly, the surplus generated during an economic upturn (when revenue exceeds expenditure) boosts financial assets.

The current debt rule takes into account the debt but not the financial assets. If, during a period of economic growth, a country wants to build fiscal buffers for a downturn, financial assets should also be taken into account in the debt rule. In that case, the following formula could be used as the debt rule for public finances: (general government financial assets– debt)/GDP. When applied to financial assets, this debt rule would be fully compatible with the multi-year net expenditure rule supported by such bodies as the European Fiscal Board.

In fact, the OECD already includes this indicator in the statistics that it produces for its member countries. The same figures can be found in the statistics produced by Eurostat for European Union Member States.

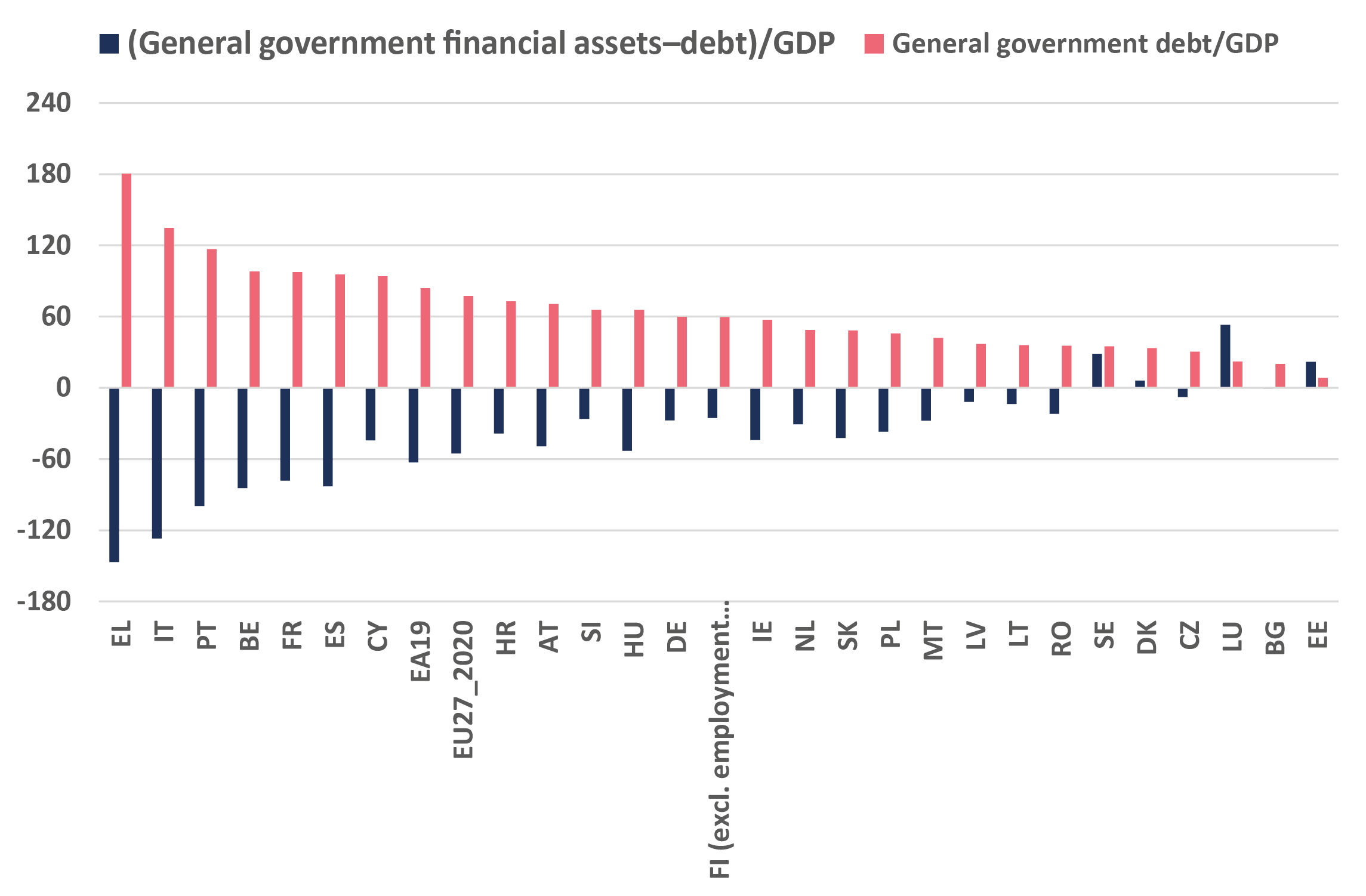

Figure 1. (Financial assets–debt)/GDP and debt/GDP, EU27, euro area 19 and Member States, year 2019.

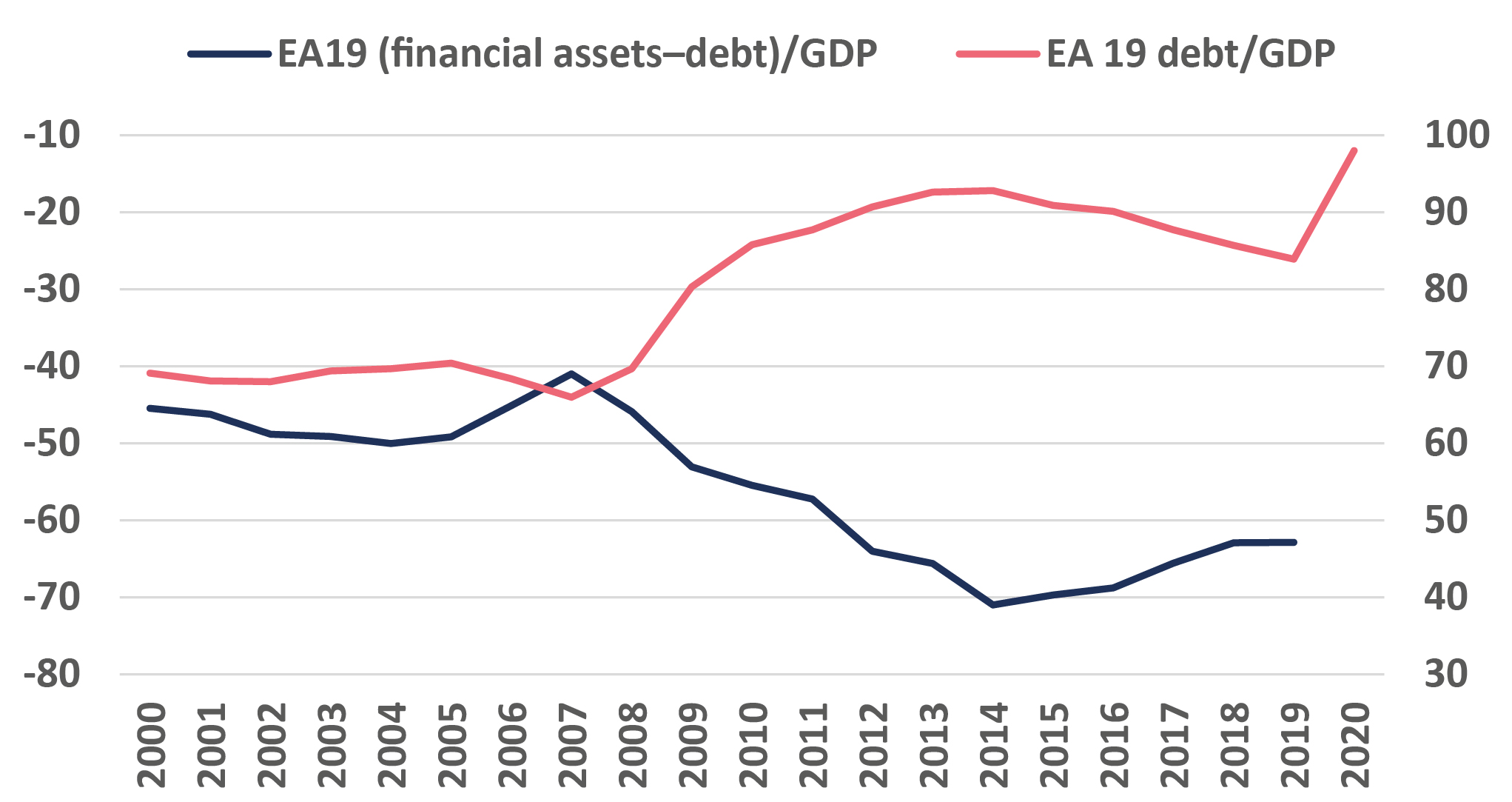

Figure 2. (Financial assets–debt)/GDP and debt/GDP, euro area in the period 2000–2020.

Figure 1 shows EU Member States, their debt-to-GDP ratio from highest to lowest and the value of the indicator (financial assets–debt)/GDP. The indicator values go almost hand in hand. The ranking of the countries is very similar in both indicators. The value of the Pearson’s correlation coefficient describing the order of the countries is 0.94. Figure 2 shows that the indicator used here does not vary in time more than the debt/GDP ratio.

Not all assets are contained in the financial assets. For example, real assets (such as buildings and land areas) are not included. It has also been stated in the debate on EU rules that there is no desire to include non-liquid assets in financial assets. From this perspective, an indicator including financial assets would be acceptable as a debt rule for EU Member States. When financial assets are lower than the debt, negative values are assigned to the indicator.

Debt/GDP ratio and the (financial assets–debt)/GDP indicator are also linked to each other in terms of their values. The figure of about –35% of the latter indicator is associated with the 60% value of the debt/GDP ratio. A suitable benchmark can thus be calibrated for the debt rule incorporating financial assets starting from the more familiar debt/GDP indicator value.*

The indicator examined here could act as a debt rule for EU Member States encouraging them to build surpluses during an economic upturn for use as buffers during a downturn. Additionally, the sales of state-owned shares generating dividend income are shown in this indicator. The sales are not shown in existing rules even though in the long term, dividend income enhances the sustainability of general government finances.

General government fixed capital (excl. non-liquid assets such as buildings, roads and waterways) could also be added to the general government financial assets considered in this debt rule. In that case, general government investments in fixed capital (incl. research and development) would be positively considered in the debt rule. In addition to investments in fixed capital, this debt rule could also take positive account of educational and climate investments.

*The following regression formula can be used to convert the desired debt/GDP ratio to the corresponding value of (financial assets–debt)/GDP indicator: (financial assets–debt)/GDP = 30.8–1.1x debt/GDP.

Postscript

The current debt/GDP indicator value is impacted by the business cycle, as cyclical fluctuations are built in the GDP. In fact, not even the (financial assets–debt)/GDP indicator is perfect in this respect. It should be added, however, that in this indicator, the cyclical conditions affecting the denominator’s GDP are also reflected in the valuation of the shares included in the numerator’s financial assets. The impact of cyclical fluctuations will be reduced further if general government fixed capital is partially added to the assets as discussed above.

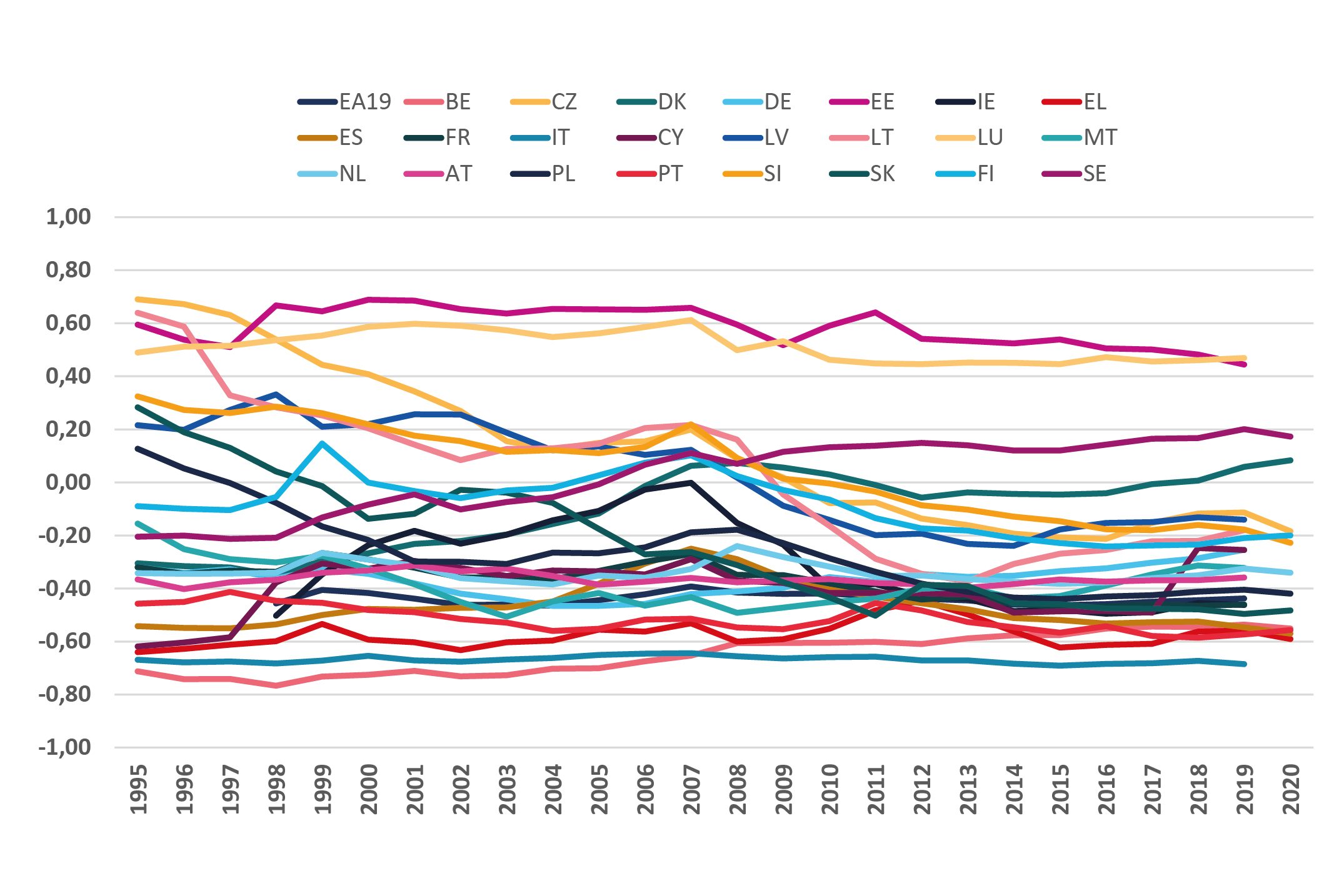

If the impact of the business cycle on the debt rule is to be further reduced, the third option would be to relate the general government (financial assets–debt) variable to the general government (financial assets+debt) variable. As shown in Figure 3, this indicator is assigned values between 1 and –1 and it is quite stable for each country.

Focusing on the analysis of (net) debt sustainability would lead to an even longer-term debt rule, as proposed by Paul de Grauwe to the European Parliament in 2021.

Figure 3. General government (financial assets–debt)/(financial assets+debt) euro area 19 and euro countries 1995–2020.